Investor Readiness Scorecard: What VCs Look For

Click on image to enlarge

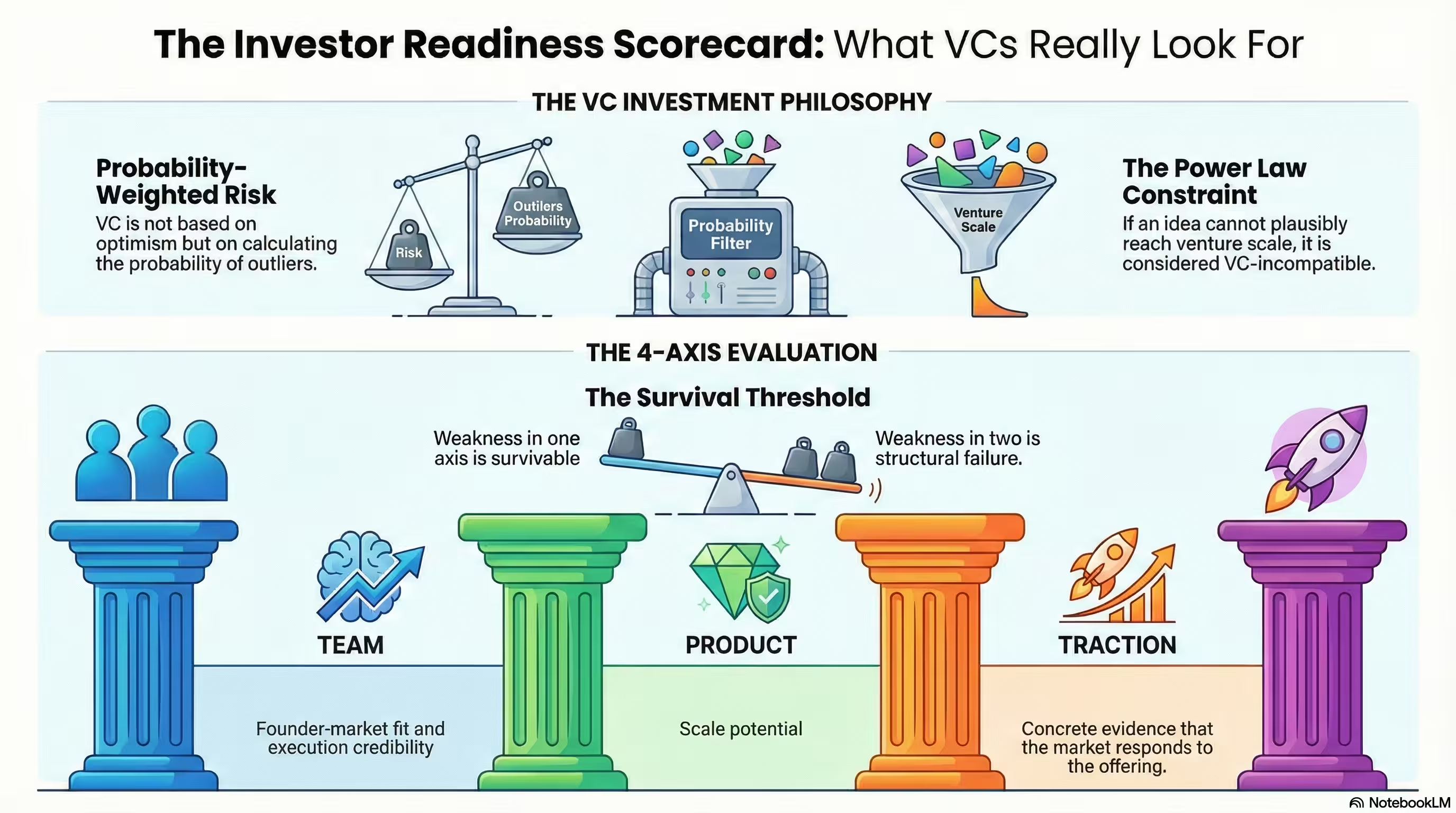

Venture capital is not optimism. It is probability weighted risk. Investors are not paying for effort, vision, or a "cool product." They are paying for a credible path to an outcome big enough to return the fund.

At pre-seed and seed, VCs know the product will change, the market will evolve, and the team will learn. What they evaluate is not certainty - it's trajectory: whether your startup has the ingredients that tend to produce outlier outcomes.

That evaluation is far more structured than most founders expect. The best investors run pattern recognition plus a scorecard logic: a set of critical axes where weakness can be survivable - but too many weaknesses become fatal.

The Power Law Constraint

Funds require outliers. The venture model is constrained by a power law: a small number of investments generate the majority of returns. That means VCs must believe your company can plausibly reach venture scale.

If your business cannot become large enough, fast enough, with strong enough margins - it might still be a great business. It just might not be a venture business. That's not an insult. It's a model constraint.

VC Compatibility Test

Can this company plausibly become a $100M+ revenue business with a defensible advantage, within a timeframe that fits a fund? If the answer is "not really," investors will pass even if the idea is solid.

This is why "we'll capture 1% of a huge market" doesn't work. Investors want a path from a narrow wedge to a large expansion, not a top-down fantasy.

The 4 Core Evaluation Axes

Team

Founder-market fit, execution credibility, and the ability to recruit. Investors are underwriting learning speed as much as current skill.

Market

Size, growth, timing, and whether the market structure allows a breakout winner. Great markets pull companies forward.

Product

Differentiation, defensibility, and clear user value. "Better UX" is rarely enough. Investors look for wedges, not wishful thinking.

Traction

Evidence that the market responds: retention, usage intensity, revenue signals, pipeline quality, or strong pilot commitments.

Weakness in one axis is survivable. Weakness in two is structural. Weakness in three is usually a pass - unless the fourth axis is extraordinary.

Axis 1: Team - The "Unfair Advantage" Question

At early stages, the team is often the dominant factor. Investors ask: Why you? Why are you uniquely positioned to win this market?

Founder-market fit can come from domain experience, network proximity, or a track record of building and shipping in similar conditions. A strong founder can enter a hard market because they understand the buyer deeply.

What VCs listen for

- A clear reason you care about this problem beyond "it seems big."

- Proof you can execute: shipped products, results, leadership, or growth stories.

- Signals you can recruit: credibility, taste, and ability to attract talent/advisors.

- Coachability: not "agreeable," but fast learning under pressure.

The hidden team metric is decision quality. Investors watch how you think. Do you use evidence? Do you update beliefs when wrong? Do you explain tradeoffs clearly? The pitch is a proxy for how you'll run the company.

Axis 2: Market - The "Tailwinds" Question

A mediocre team in a great market can still win. A great team in a weak market will struggle. Investors look for tailwinds: regulatory shifts, new tech, cost drops, behavior change, or distribution unlocks that make "now" the right time.

Market is not only size. It's also structure. Are there clear buyer budgets? Is there an incumbent that is vulnerable? Is the market fragmented (opportunity) or winner-take-all (hard but valuable)?

The best founder answers are specific: who pays, why they pay, and what changes in the world made this possible now.

Axis 3: Product - Differentiation That Matters

Investors are skeptical of "we're building X but better." Better rarely wins unless it is meaningfully better in a dimension buyers value: speed, cost, compliance, workflow integration, reliability, or outcome quality.

The strongest wedge is often not feature-based. It's: distribution (you can reach buyers cheaper), data (you can improve outcomes), workflow ownership (you sit in the daily habits), or regulatory advantage (you can do what others can't).

A practical differentiation test

If a competitor copies your product in 90 days, do you still win? If not, your differentiation is not defensible yet - it's a feature set.

Axis 4: Traction - Signals Over Stories

Traction is not always revenue at pre-seed. But it must be a credible signal that the market responds. Strong signals include: high retention, intense usage, paid pilots, signed LOIs, repeatable outbound conversion, or a waiting list that converts.

Investors are allergic to vanity metrics. They want to know: does the product create behavior that is hard to fake?

Investors fund momentum, not potential.

You don't need perfect numbers. You need proof that reality is moving in your direction.

Run Your Analysis ->The "Investor Readiness" Checklist (Quick Version)

- Pitch clarity: Can you explain the buyer, pain, and wedge in under 30 seconds?

- Market logic: Can you show a credible wedge + expansion strategy?

- Moat direction: Is defensibility increasing over time (data, workflow, distribution, network)?

- Traction proof: Do you have at least one hard-to-fake signal?

- Execution plan: Do you know your next 90 days in concrete steps?

- Asks: How much money, for what milestones, and why that's the right amount?

The goal of fundraising is not to "sound impressive." It's to reduce investor uncertainty with structured evidence. If you can do that, you won't need hype - you'll have credibility.

Keep Reading

- Why 90% of Startup Ideas Fail Before Launch -structural weaknesses that predict failure

- TAM Is a Vanity Metric -the market signals that actually matter

- The Brutal Truth About Product-Market Fit -real PMF signals vs. vanity metrics

Want your investor readiness score?

Run a startup idea validation and get an investor-style scorecard across team, market, product, and traction.